Coronavirus and your HMO and the economic outlook – a summary

This piece is taken from my Youtube video which you can watch here – https://www.youtube.com/watch?v=a9QFmQC9dtk&t=49s

Coronavirus and your HMO and the economic outlook – a summary

There is no crystal ball in property. All we can do is educate ourselves and learn how to read the signs. Financial education will help you understand what is the best course of action for you to take for your circumstances at this time.

Being an experienced investor (I’ve been investing for over 23 years) has shown me two things

1) People always need homes

2) There are always opportunities to serve others and make money

Financial education will help you protect yourself, your tenants, your properties and your business. It will also help you make wise decisions. There are some key economic factors that we as investors need to understand

- Inflation

- Interest rates

- Debt and borrowing ratios

- Cashflow

- Spending

These apply to nations, business and property. National income and turnover is called GDP – Gross Domestic Product. The current biggest threat to our GDP right now is Coronavirus. Tax receipts will go down, and spending will go up – leading to more borrowing. Will this lead to higher inflation? What will that mean to us as investors?

3) Only 34% of the UK’s income is from tax receipts. That means that spending, leverage and borrowing are fuelling the economy. Tax receipts will go down and spending will go up due to Coronavirus. Equally the government has borrowed huge amounts of money to get us through this time, leading, inevitably to higher inflation (eventually).

Over time, this will affect you if you are a borrower or have leveraged your property with debt because inflation erodes debt. It also causes prices to rise and house prices to increase. This could be good news for investors. However, if the government raises interest rates to slow the rate of inflation, there will be an impact on mortgages. Monthly rates will go up and reduce cashflow.

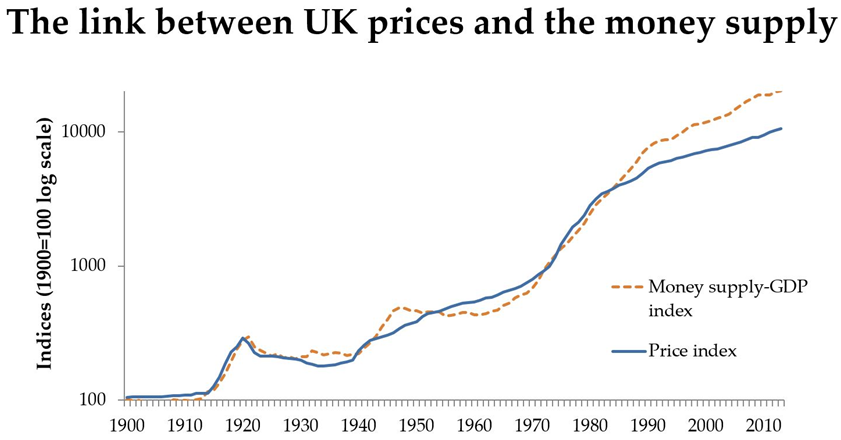

4) House prices are more linked to money supply than demand.

- The government has recently started a further round of Quantitative Easing recently which has added another £500bn to the money supply. What will this do to inflation in the long run? If this money starts to circulate (as it should) then inflation will be the result. This will result in higher house prices and capital growth.

5) What does this mean if you invest in HMOs?

Use a cashflow forecast to create a tight handle on your income and expenditure.

Keep a tight control of your finances.

Communicate with your tenants regularly to ensure cashflow – they still need a home, and you need an income. Create a compromise on rents so that you can both get what you need.

Now is the time to plan and learn so that when the opportunity arises you are ready to pounce!

6) Keep up to date with advice and information from the government. Set aside a few minutes per day to understand what the advice means for you. Reduce overwhelm by addressing your immediate issues and then blocking out time to look at the stuff that’s important but less urgent.

7) Making Decisions during Coronavirus

Make decisions calmly and on a risk-based scenario (impact and likelihood)

Analyse how you are making decisions (fear based or information –based)

Sound out any particularly big decisions with a friend, business colleague, mentor or trusted individual.

Create a Plan B should the worst happen

Set time aside every day or other day to stand back and analyse key performance metrics (income/ expenditure/ room sales/ rental income/ arrears).

Don’t bury your head in the sand! Reach out if you need further help.

8) Should I carry on with my HMO purchase?

If you are currently buying, consider renegotiating price or delaying purchase

Worth keeping any finance deals on the table as they could be harder to get later

Soon there will be some great deals

Work with investors as savers are losers

If you are currently buying – take a RISK BASED APPROACH – do the maths on the deal

Keep an eye on auctions

Otherwise wait

9) Your Own Health and Wellbeing as an Investor

Look after yourself and your family

Take action and use tools to run your business properly

Make sensible decisions

Be responsible, not selfish

Be patient and have faith

If all else fails – remember, this too will pass